Iconic American department store operator Sears Holdings Corporation filed for Chapter 11 bankruptcy protection, becoming easily the highest-profile casualty of the "Retail Apocalypse" to date. According to a press release delivered on Oct. 15 by the company, Sears "...has received commitments for $300 million in senior priming debtor-in-possession ("DIP") financing from its senior secured asset-based revolving lenders and is negotiating a $300 million subordinated DIP financing with ESL Investments, Inc. ("ESL"). ESL is the Company's largest stockholder and creditor, and Edward S. Lampert is ESL's Chairman and Chief Executive Officer. Subject to Court approval, the DIP financing is expected to improve the Company's financial position immediately and support its operations during the financial restructuring process."

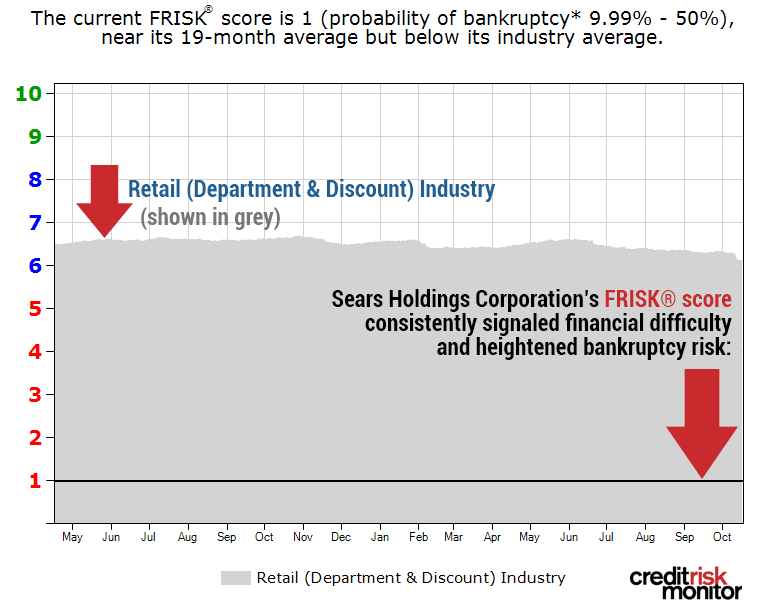

The CreditRiskMonitor FRISK® score tabbed Sears for several years as a candidate for eventual failure - for more than 24 consecutive months, the Chicago-based company sat at a FRISK® score of "1," which is defined as a company showing a 10-to-50% probability of bankruptcy within 12 months' time.

Download the free report to learn more.

Ready to learn more?

Our FRISK® score model incorporates four powerful risk inputs:

- “Merton”-type model of stock market capitalization and volatility

- Financial ratios, including those used in the Altman Z”-Score Model

- Bond agency ratings from Fitch, Moody's, and DBRS Morningstar

- Website click pattern data from CreditRiskMonitor® subscribers, representing key credit decision-makers at more than 35% of current Fortune 1000 companies plus thousands of other large companies worldwide

Since the start of 2017, the FRISK® score’s rate of success in capturing public company bankruptcy is 96%. In any given year, you can count on one hand the times we miss – and in those outlier cases, the circumstances deal with unusual, unforeseen events such as natural disasters and CEO fraud.

Download the free report to learn more.

About Bankruptcy Case Studies

CreditRiskMonitor® Bankruptcy Case Studies provide post-filing analyses of public company bankruptcies. Our case studies educate subscribers about methods they can apply to assess bankruptcy risk using our proprietary FRISK® score, robust financial database, and timely news alerts.

In nearly every case, a low FRISK® score gave our subscribers early warning of financial distress within a one-year time horizon. Our proprietary FRISK® score predicts bankruptcy risk at public companies with 96% accuracy. The score is formulated by a number of indicators including stock market capitalization and volatility, financial ratios, bond agency ratings from Moody’s, Fitch and DBRS, and crowdsourced behavioral data from a subscriber group that includes 35% of the Fortune 1000 and thousands more worldwide.

Whether you are new to credit analysis or have decades of experience under your belt, CreditRiskMonitor® Bankruptcy Case Studies offer unique insights into the business and financial decline that precedes bankruptcy.