Movie theater operators endured financial strains beyond any earthly expectations coming into 2020 amid the economic shutdowns caused by the coronavirus pandemic. CreditRiskMonitor's proprietary crowdsourcing data, harvested from specific click data and patterns, shows that subscribers have been closely monitoring public companies AMC Entertainment Holdings and Cineworld Group. Despite a seemingly positive outlook for Hollywood in 2021, risk professionals continue to exhibit tremendous concern about some of the biggest movie theater chains in the world – we will explain why these operators should remain under a watchful eye.

The Virtual Credit Group

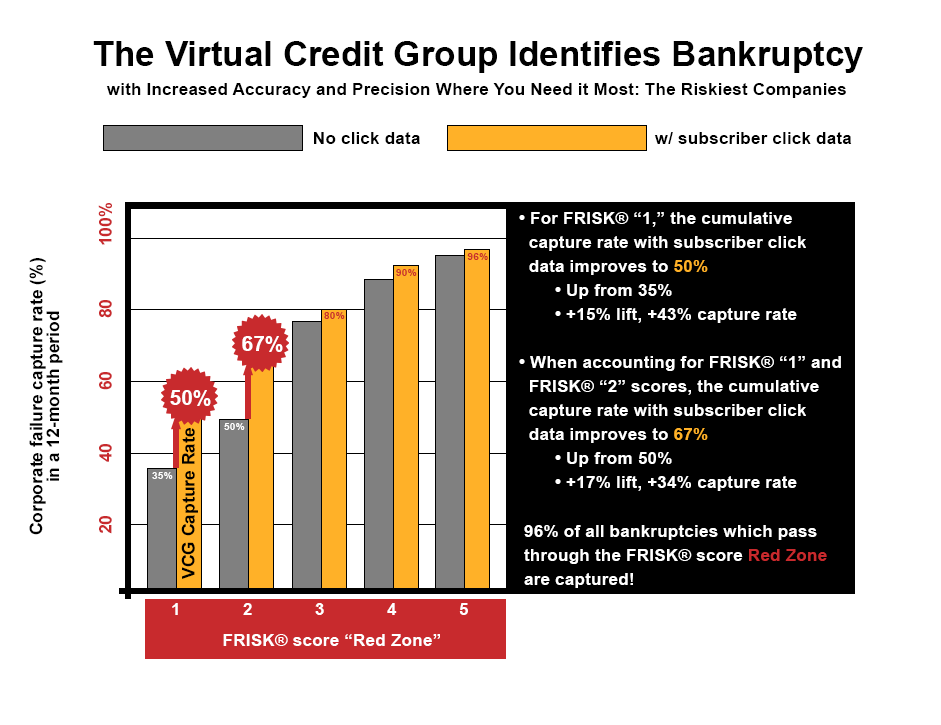

When financial risk professionals are concerned about a public company, we’ve found that their research behaviors will shift and when considered in the aggregate are predictive of corporate bankruptcy. With nearly 20 years of history of tracking the anonymous click activities of its subscribers, including professionals from nearly 40% of the Fortune 1000, CreditRiskMonitor has been able to produce a daily, independently predictive analytic of near-term bankruptcy risk, which has been integrated into the 96%-accurate FRISK® score to enhance timeliness and accuracy. As shown in the graphic below, bankruptcy capture rates have benefited materially from the inclusion of this proprietary data and sentiment analysis.

Think of subscriber crowdsourcing as a “Virtual Credit Group,” a hive mind that will help in the identification of highest risk counterparties. Risk professionals are responsible for the extension of trade credit, which represents over 25% of corporate debt within the United States. Trade credit financing is typically interest-free or even offered at a discount for expedited payment in comparison to alternative sources of working capital financing such as bank or third party (hedge fund) loans, notes, and bonds. Moreover, many corporations that are starting to show elevated risk are unable to secure bank financing due to poor performance, poor leverage ratios, or a lack of good cash flow metrics. Finally, the need to tap trade credit financing is highest in points of distress when interest expenses are most burdensome. CreditRiskMonitor’s crowdsourced usage behavior specifically identifies this shift in aggregate sentiment among the issuers of trade credit and therefore assists in the monitoring of the most critical situations when trade credit-based working capital liquidity can dry up. Recently, concerns have been elevated for both AMC Entertainment and Cineworld Group, which are reflected in their respective FRISK® scores.

Buying Some Time

Shutdowns made AMC Entertainment and Cineworld Group print a lot of red ink last year, and both companies quickly went into survival mode. Each aggressively cut costs and raised debt and equity capital to sustain liquidity. AMC Entertainment’s stock performance improvement, as a celebrated Meme Stock, allowed the company to seek investor approval for a share authorization, according to Reuters. The company’s management discussion and analysis (MD&A) section of its 2020 annual report explained that "the liquidity we have raised has substantially extended our liquidity runway" but also that "our current cash burn rates are not sustainable." Adding to the uncertainty of 2021 involved the following disclosures:

“Commencing in 2021, our cash expenditures for rent are scheduled to increase significantly as a result of rent obligations that had been deferred to 2021 and future years...the new debt we have issued or that has been committed, together with the higher interest rate payments that will be required in the future but have largely been deferred, will substantially increase our leverage and future cash requirements.”

With a bottom-rung FRISK® score of "1", AMC Entertainment carries a 10-to-50% greater risk of bankruptcy over the coming 12 months than the average public company. Its elevated financial leverage and overall operating performance, therefore, must be monitored closely. Although liquidity has been secured, if movie attendance does not meaningfully improve, rent concessions and deferred interest costs could become insurmountable obstacles.

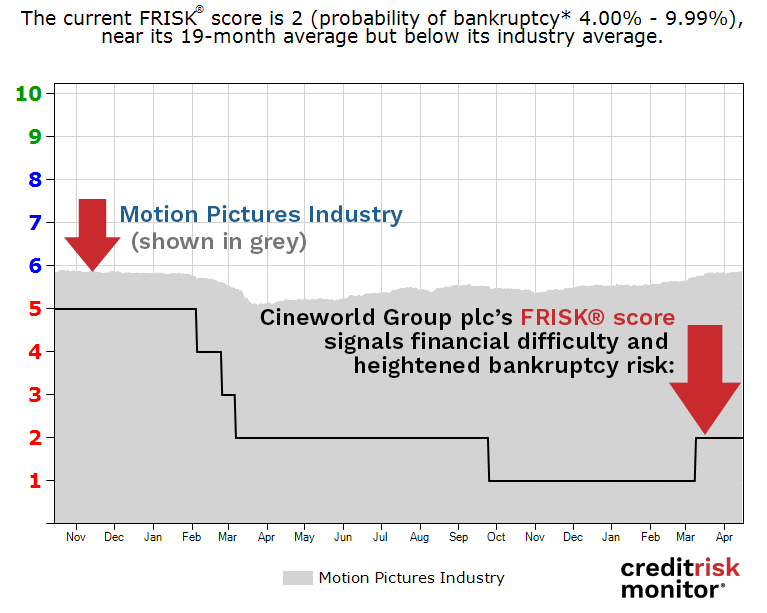

Cineworld Group has a marginally better FRISK® score of "2," indicating a bankruptcy risk of 4-10%, bigger than average, yet is certainly under the weight of similar adverse business conditions.

Cineworld Group reported an aggressive burn rate for FY20, and while it still managed to secure financing, a cash crunch is not entirely off the table. Cineworld would request shareholders to approve its debt ceiling, according to Reuters. Two unsettling factors remain, however – Cineworld Group's total liabilities are five times larger than its market capitalization and total debt-to-assets is 81%. As the company still has an uncertain future, its FRISK® score and reported financial trends must be evaluated with great care.

Lastly, streaming video content is also an industry headwind that extends beyond COVID-19 that will continue to pressure long-term attendance. On balance, risk professionals are monitoring both AMC Entertainment and Cineworld Group, and for good reason as the trajectory of attendance recovery will likely determine whether these companies survive…or not.

Bottom Line

CreditRiskMonitor's FRISK® score, enriched by subscriber crowdsourcing, indicates that there is still material risk in the movie theater industry. While it is challenging to predict the future, the FRISK® score is providing specific warning signals on AMC Entertainment and Cineworld Group -- and credit managers are taking heed and monitoring extensively. Contact CreditRiskMonitor today to see how we can help you track the ongoing risk at these movie theater operators and in other industries globally as the COVID-19 pandemic continues to play out in unexpected ways.