Keep your brains about you: if it looks like a zombie, acts like a zombie, and reports like a zombie, it is probably a zombie.

A “zombie” company is a company that is, at best, able to generate just enough earnings to support its interest expenses, i.e. Interest Coverage Ratio of one or less. The IMF recently addressed this issue, explaining that widespread zombification across sectors and industries has delayed an enormous flood of bankruptcies:

“Unprecedented policy measures helped avoid a wave of insolvencies, at least temporarily. But risks remain of corporate debt overhang and zombification of firms if untargeted support is prolonged and of a wave of insolvencies if support is removed abruptly."

CreditRiskMonitor enables procurement and supply chain professionals to identify zombie firms using the FRISK® score combined with financial statement spreads and Management’s Discussion & Analysis (MD&A) report features. Below we explain how zombie counterparties can cause supply disruptions and the steps to mitigate risk exposure.

Zombie Supplier Problems

As supply chains face cost inflation and interest rates rise, zombie companies are about to break the proverbial dam. For more than a decade, zombie companies worldwide have been able to refinance existing borrowings without the need for repayment. Such maneuvering has kept struggling companies "alive" but simultaneously left them with limited discretionary cash flow available to invest in R&D, new technologies, infrastructure, maintenance capital expenditures, and strategic mergers and acquisitions. Certain zombie companies will even resort to unsustainable tactics, such as borrowing additional debt, relying too heavily on supplier financing, or selling assets to fund interest payments. This optionality diminishes during times of crisis and ultimately results in supplier financial stress.

Among the top reasons for supply chain disruptions, supplier financial stress will frequently cause one or more of the following issues:

- Product quality issues

- Production slowdowns

- Inventory and critical part shortages

- Transportation disruptions

- Supplier bankruptcy liquidations

Frequently Scan for Zombies

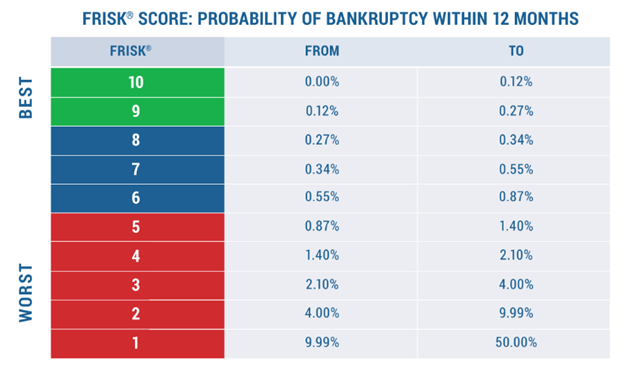

The CreditRiskMonitor FRISK® score funnels the riskiest zombie companies into scores of "5" or below on the "1" (highest risk)-to-"10" (lowest risk) score, into the "red zone” indicating above-average bankruptcy risk relative to public company long-term average. The FRISK® model incorporates financial statement ratios; stock market performance; bond agency ratings from Moody’s, Fitch, and DBRS Morningstar; and the aggregate risk sentiment of our subscriber base. The non-linear combination of these data sets allows the score to capture a baseline of 96% of all publicly traded companies that eventually go bankrupt within its high-risk category at least three months before they file.

As previously stated, zombie suppliers will characteristically have an interest coverage ratio of one or less. At CreditRiskMonitor, we calculated the interest coverage ratio using earnings before interest, taxes, depreciation, and amortization over net interest expenses. In 2021, CreditRiskMonitor released a Bankruptcy Case Study on offshore oil and gas drilling services operator Seadrill Ltd., showing its interest coverage ratio below 1x for five consecutive years before failing. Review our High Risk Reports to see other examples of poor interest coverage ratios, which include auto & truck parts supplier Cooper-Standard Holdings Inc., biotechnology & drug manufacturer Lannett Company, Inc., and business services firm Team, Inc.

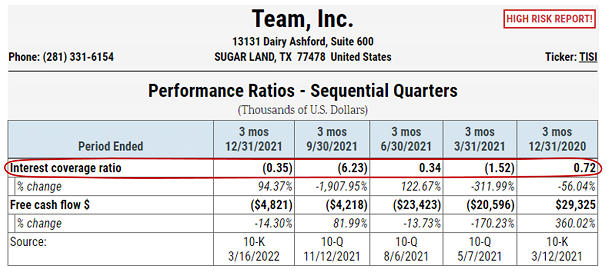

In Team Inc.’s CreditRiskMonitor report, subscribers can view performance ratios to show its interest coverage ratio trend over the last five sequential quarters.

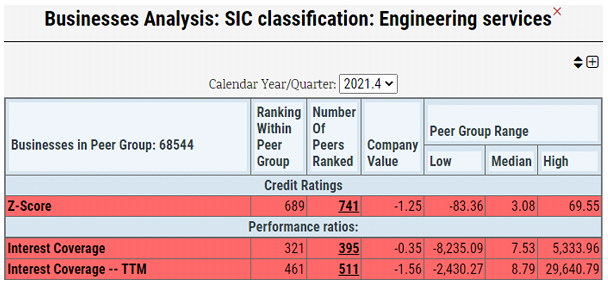

Navigating to the peer analysis section, Team, Inc. also ranks in the bottom quartile of industry comparables with its negative interest coverage ratios. Subscribers can access the ranked peers section to quickly identify other zombie firms in the industry.

Zombies will sometimes have high short-term debt as a percentage of their total debt. On top of near-term maturity refinancing, credit revolvers and term loans have variable rate interest that is also affected by higher base interest rates. For instance, Unique Fabricating Inc.’s CreditRiskMonitor report hits all the marks for being a zombie vulnerable to bankruptcy:

- A FRISK® score of “1,” indicating 10-to-50x higher than average bankruptcy risk

- An interest coverage ratio under one, reflecting inadequate debt servicing

- All debt is short-term due to accelerated maturities

- All issued debt has variable-interest-rate payments

Also to be considered is the MD&A section found within Form 10-Q and 10-K filings, easily accessible in CreditRiskMonitor company reports. Unique Fabricating specifically disclosed covenant red flags in its latest Q4 2021 filing:

"On March 11, 2022, the Company entered into the Sixth Amendment to Forbearance Agreement, which extends the Forbearance Period from March 11, 2022, to May 30, 2022. During the extended Forbearance Period, the Company expects it will continue to be able to borrow under the revolving line of credit, subject to availability and satisfaction of certain other conditions. The Company has used and intends to use the forbearance period to continue negotiations with the Lenders to enter into an amendment and waiver to cure the defaults."

By being a CreditRiskMonitor subscriber, risk evaluators can quickly identify zombie suppliers and understand whether they have longevity or if they will simply cause more problems than they are worth.

The Supply Chain Cure

Supply chains frequently desire to maintain their relationships with existing suppliers, vendors, and third parties even in trying times. Sticking with the devil – or zombie company – that you know is the easier play, but is it the correct one? If your counterparty is a zombie, it is critical to create an action plan today to mitigate the aforementioned risks, which can include:

- Buying additional merchandise early to provide your supplier with cash flow

- Grow warehouse stockpiles or safety stocks for inventory runway

- Engage in a supply chain financing program to improve supplier working capital

Supplier bankruptcy can be an unavoidable outcome, however, which might require alternative methods such as:

- Implementing a dual sourcing strategy

- Offering bankruptcy financing or acquiring the supplier

- Sourcing from an alternative supplier

- Purchasing disruption insurance

- Taking the process in-house

Bottom Line

Supply chain and procurement professionals must always be reviewing their Tier 1, 2, and 3 suppliers. Depending on the size of your company, it is likely you could have anywhere from a couple to several dozen zombie vendors as counterparties. As the risk of another global recession builds, any subscribers who are not currently reviewing their supply chains for zombies should do so immediately. Contact CreditRiskMonitor to learn how you can use the FRISK® score and other CreditRiskMonitor report features to protect your company from bankruptcy-prone zombies.